Six Takeaways from Goldman Sachs’ High Net Worth Alternative Investor Survey

Six Takeaways from Goldman Sachs’ High Net Worth Alternative Investor Survey

Karma Martell

Karma Martell, Founder of KarmaCom, is a seasoned professional business commentator, writer, and marketer, and serves as virtual CMO for International Wealth Tax Advisors.

Contact IWTA

To schedule an introductory phone conference with IWTA founder Jack Brister simply click here. Email IWTA at bloginquiries@iwtas.com Or call the IWTA New York City office at 212-256-1142

Latest Posts

Find Previous Posts

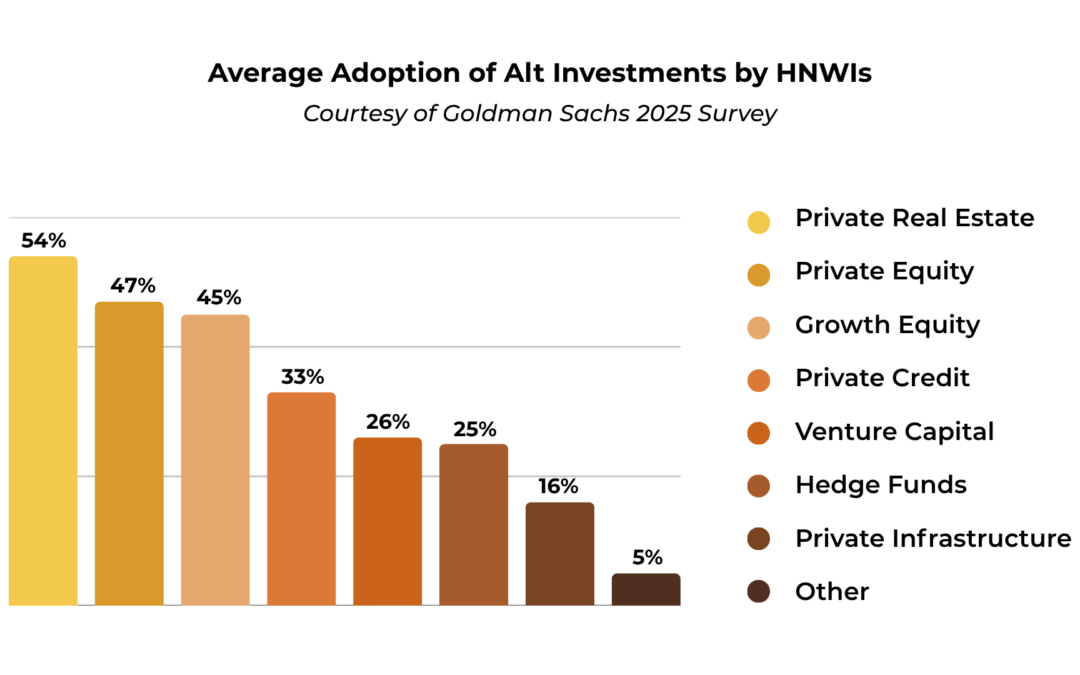

A new report from Goldman Sachs Asset Management, “Opening the Door to Alternatives,” summarizes the key findings from their survey of 1,000 high-net-worth (HNW) U.S. investors ($1 million or more) regarding their engagement with private markets.

Alts assets allocations rise with the size of the investment portfolio.

1. Asset Size Tracks Adoption

Alts adoption rates soar with net worth. 80% of households with $10 million or more in investable assets are allocating to alternatives.

2. Millennials Lead the Trend

Millennials show the highest allocation to alternatives with at 20% of their portfolio. Gen X (11%) and Baby Boomers (6%) are slower to adopt. Millennials’ prime motivations are performance and access to innovation.

3. Cash is Still King

Despite rising interest in alternatives, wealthy households still maintain high cash balances, averaging 20% of their net worth across all tiers.

4. Risk vs. Reward

While a majority (56%) of investors label alternatives as “high risk,” the primary drivers for those invested are performance (46%) and diversification (34%).

5. The Advice Gap

Only 41% of those surveyed discussed alternatives with their financial advisors. Millennials often cite social media as a source of information, while Baby Boomers rely on traditional financial media. Our question: is AI filling part of that gap?

6. Real Estate Starter Kit

Private Real Estate is the go-to alternative for individuals with under $5 million in investable assets. Usage broadens to include Private Equity and other alternatives in higher wealth tiers.

Click here to see a larger version of the bar chart.

Related Articles

The New Wealth Class Is Betting on Alternatives — And Triggering a Tax Crunch

Younger, affluent investors are increasingly turning to alternative investments, and may overlook the complex tax consequences that arise from these investments, including K-1 and pass-through income, which can lead to tax and estate planning headaches.