The New Wealth Class Is Betting on Alternatives—And Triggering a Tax Crunch

Younger, affluent investors are increasingly turning to alternative investments, such as private equity, venture funds, real estate syndications, and even collectibles. In their quest for diversification and outsized returns, they may overlook the complex tax consequences that arise from these investments, including K-1 and pass-through income, which can lead to tax and estate planning headaches.

The Wealth Transfer Is Here: Young Affluent Investors Are Gaining Ground

A massive generational wealth transfer is underway, with $84 trillion projected to move to Millennials and Gen Z by 2045. And while Boomers currently control approximately 52% of US wealth, Millennials stand to inherit the most money of any generation over the next 25 years.

And this generation invests differently than their parents or grandparents. Growing up in a landscape shaped by the 2008 financial crisis, rapid tech innovation, and low trust in traditional institutions, younger investors are more comfortable with higher risk, less liquidity, and digital-first platforms. While older generations built wealth through steady exposure to public markets, homeownership, and retirement accounts, millennials are drawn to private equity, venture capital, crypto, and alternative assets not just for diversification and potentially higher returns, but also because these investments align with their values—like backing innovation, sustainability, or emerging technologies.

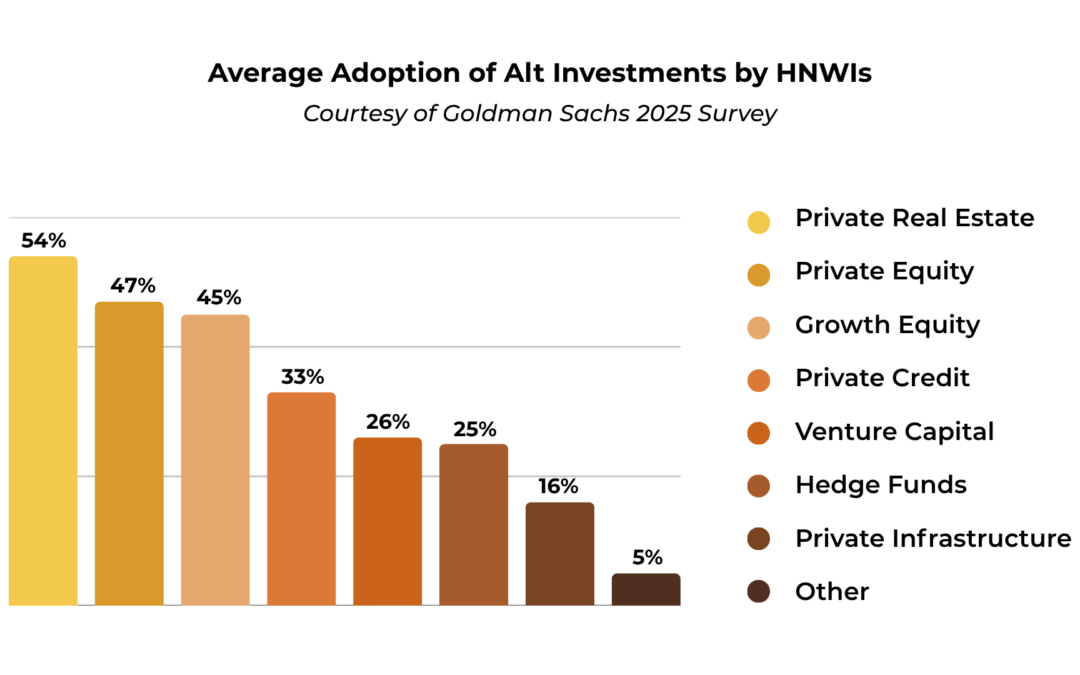

The Hidden Cost: Alternative Investments Come With Tax Headaches

As this generation looks beyond the traditional stock and bond markets to build their wealth, what are the tax consequences for younger investors, and are they prepared?

Young HNWI are drawn to alternative assets for growth and diversification—but often lack integrated tax planning infrastructure. Without proactive tax and legal guidance, they risk missed savings, surprise liabilities, and execution roadblocks.

Private Equity and Real Estate May Involve K‑1 Complexity and Pass‑Through Income

When investors participate in private equity, real estate syndications, or other partnerships, they receive a Schedule K‑1, which reports their share of income, deductions, and credits. K‑1s often arrive late—after April 15—forcing investors to file extensions, estimate taxes, or risk penalties and interest. Additionally, income reported on K‑1s may come from multiple states, triggering multi-state tax filings even for passive investors. Crucially, pass-through income can be taxed at ordinary income rates, not the more favorable capital gains rates, reducing after-tax returns.

Alternative Investments and Unrelated Business Taxable Income

Alternative investments held inside self-directed IRAs (SDIRAs) may generate Unrelated Business Taxable Income (UBTI)—particularly when the IRA uses debt-financing or operates a business within the investment. For example, if a leveraged real estate syndicate is inside an IRA, the debt-financed portion of income becomes UBTI and is taxable within the IRA. Once the IRA’s UBTI exceeds $1,000, the custodian must file Form 990‑T, and taxes are paid from IRA assets—eroding returns and complicating tax planning.

Estate Planning and Valuation Challenges

Alternative assets such as private equity, real estate syndications, and collectibles are illiquid and hard to value, complicating estate planning and gifting. Accurate appraisals are needed for tax purposes, and aggressive valuation discounts may draw IRS scrutiny. Many tax-advantaged strategies—like Grantor Retained Annuity Trusts (GRATs) or Intentionally Defective Grantor Trusts (IDGTs)—become harder to deploy effectively without careful structure and valuation support.

Phantom Income and Capital Gains Timing

Private investments often generate imputed or phantom income—taxable income without actual cash distributions—potentially triggering estimated tax obligations and cash-flow mismatch. Conversely, realizing capital gains may be delayed by an asset’s illiquidity, leading to timing issues for tax liabilities and missed opportunities to harvest losses. Furthermore, passive activity loss rules may restrict the use of reported losses, limiting offset potential.

Multi-State and International Reporting Burdens

Investments that include assets or activities in multiple U.S. jurisdictions may create state filing requirements across several states due to nexus—necessitating multiple tax returns and compliance efforts. Moreover, non-U.S. investors must navigate additional complexities, such as Foreign Investment in Real Property Tax Act (FIRPTA) withholding, effectively connected income (ECI) filings, estate tax exposure, and withholding treaties. See our article about the 16th Amendment and Moore vs the United States.

Without proactive tax and legal guidance, these younger investors risk missed savings, surprise liabilities, and execution roadblocks. Jack Brister and his capable team know U.S. and international tax statutes inside and out. We’re here for a consultation, an evaluation, and to serve as a trusted advisor and accounting partner. Whether you call Detroit, Dublin or Dubai your home, if you have investments, business, family or residences in the U.S., we can help.