Sens. Joe Manchin (D-W.Va.) and Krysten Sinema (D-Ariz.) are in discussions over a climate and tax package, while the Biden administration is launching a pilot program dealing with rural wastewater.

This is Overnight Energy & Environment, your source for the latest news focused on energy, the environment and beyond. For The Hill, we’re Rachel Frazin and Zack Budryk. Someone forward you this newsletter? Subscribe here.

Us inheritance tax for non us citizens Manchin, Sinema discussing reconciliation

Sen. Joe Manchin (D-W.Va.) says he is exchanging materials with Sen. Kyrsten Sinema (D-Ariz.) to help her better understand the broad tax reform and climate bill he negotiated with Senate Majority Leader Charles Schumer (D-N.Y.) and that he is open to her suggestions as Democrats seek 50 votes to put the bill on the floor.

Manchin finally got a chance to speak to Sinema after lunch Tuesday, when she was scheduled to preside over the chamber.

Manchin was tight-lipped about the details of the conversation but made clear that he’s willing to consider changes she might want to make to the deal, which would raise $739 billion in new revenue over the next decade and reduce the deficit by more than $300 billion.

“We had a nice time. We had a nice time. Next?” Manchin said Tuesday when reporters pressed him for details of his chat with Sinema while she sat at the Senate dais.

Asked again to shed any light on whether Sinema will vote for the bill, which would give President Biden the biggest legislative victory of this first two years in office, Manchin said his colleague would make her own decision.

“We’re exchanging text back and forth,” he said, adding that Sinema is “extremely bright. She works hard. She makes good decisions based on facts. I’m reliant on that.”

Manchin said Schumer is “working with all the caucus” to get buy-in to get the budget reconciliation bill to the floor later this week.

Even though Sinema played a major role in negotiating the prescription drug reform component of the bill and set the broad parameters of the tax chapter, she learned about the deal at the same time as all of her colleagues and the general public — through a press release.

Manchin said he’s open to considering changes suggested by Sinema, including on a proposal to close the carried interest tax loophole, one of his priorities.

“We’re just basically exchanging back and forth whatever I have that she hasn’t seen. And our staffs are working together very closely,” he said, adding that he’s also exchanging materials relevant to the bill with other Democratic and Republican senators.

Us inheritance tax for non us citizens EPA, USDA take on rural water sanitation

The Biden administration announced plans on Tuesday to leverage financial and technical tools to ensure that historically underserved communities can access wastewater sanitation resources.

The pilot initiative, a joint effort between the Environmental Protection Agency (EPA) and the U.S. Department of Agriculture (USDA), will focus on 11 rural communities across the country where residents lack basic wastewater management.

“The America that we all believe in is a land of opportunity,” EPA Administrator Michael Regan said in a statement. “But, for historically marginalized communities from Alabama to Alaska, that opportunity is stolen when basic sanitation doesn’t work — exposing adults and children to backyard sewage and disease.”

Through the Closing America’s Wastewater Access Gap Community Initiative, the EPA and USDA will be working with Mississippi, New Mexico, North Carolina, West Virginia and tribal nations to help communities take advantage of relevant federal funding opportunities.

One such resource comes from last year’s bipartisan infrastructure bill, which provides $11.7 billion in loans and grants for water infrastructure initiatives, including wastewater management projects, the initiative’s partners said.

“President Biden has been clear — we cannot leave any community behind as we rebuild America’s infrastructure with the Bipartisan Infrastructure Law,” White House infrastructure coordinator Mitch Landrieu said.

“This includes rural and Tribal communities who for too long have felt forgotten,” he added.

About 2.2 million people in the U.S. lack basic running water and indoor plumbing, while even more live with inadequate sewage infrastructure that endangers the health of residents, according to the groups.

The new collaboration, the agencies said, will help communities access the financing and technical assistance that is available to improve wastewater infrastructure — aiming to “close the gap” for underserved populations.

The 11 communities included in the pilot program are Bolivar County, Miss.; Doña Ana County, N.M.; Duplin County, N.C.; Greene County, Ala.; Halifax County, N.C.; Harlan County, Ky.; Lowndes County, Ala.; McDowell County, W.Va.; Raleigh County, W.Va.; San Carlos Apache Tribe, Ariz.; and Santo Domingo Pueblo, N.M.

Senate Republicans have reached an agreement to pass legislation expanding benefits for veterans who are suffering illnesses due to toxic exposures, after they blocked the bill last week and sparked outrage from the veteran community — and comedian Jon Stewart.

“We expect to have an agreement on the PACT Act with amendments,” Senate Majority Leader Charles Schumer (D-N.Y.) said. “I believe it will pass and pass this evening. So, that’s very good news.”

A vote on the measure is expected early Tuesday evening.

Schumer said that the Senate will vote on three amendments to the bill, with 60 votes being needed to pass those bills. The upper chamber will then move to finally pass the bill.

The deal will also allow the upper chamber to vote on Finland and Sweden joining NATO on Friday.

The agreement comes as Republicans have been trying to find a way to end a standoff over the bill after blocking the measure by a vote of 55-42 last Wednesday.

High-tide flooding broke or tied records in three locations in U.S. coastal areas in the past year, according to data released Tuesday by the National Oceanic and Atmospheric Administration (NOAA).

This type of flooding has become increasingly frequent across the country but will likely decline this year, according to NOAA. The administration attributed the decrease to the La Niña weather phenomenon.

The increases are likely to be concentrated along the East Coast and Gulf of Mexico, where NOAA is predicting a 150 percent increase from the year 2000.

Since May of this year, three different NOAA-monitored locations have tied or broken previous records for number of high-tide flooding days. Reedy Point, Del., saw a new high of six events, while Kwajalein Island in the Pacific broke its 2021 record with four days. South Carolina’s Springmaid Pier saw 11 events, tying its 2021 high.

High-tide flooding occurs when ocean water floods into low-lying areas during high-tide periods, usually following tides of between 1.75 and 2 feet above the daily average. In years past, these events have been limited to storms, but they have recently become common during prevailing-wind changes or even full moons.

This news is brought to you by IWTA. Founded in 2015 and located on Avenue of the Americas, in the heart of New York City, International Wealth Tax Advisors provides highly personalized, secure and private global tax, GILTI, FATCA, Foreign Trusts consulting and accounting to many IWTAS.COM clients worldwide, including: Singapore, China, Mexico, Ecuador, Peru, Brazil, Argentina, Saudi Arabia, Pakistan, Afghanistan, South Africa, United Kingdom, France, Spain, Switzerland, Australia and New Zealand.

William Ackman isn’t known for his political takes. Typically, the billionaire hedge fund manager spends his time dissecting corporate financials, looking for his next high-profile investment or activist play.

But this week, the CEO of Pershing Square Capital Management found himself in the middle of a heated debate over the carried interest “loophole”—which allows private equity and hedge fund managers to reduce their tax burden on profits from fund investments. It’s a key part of the tax code that has helped make so many hedge fund managers like Ackman billionaires in the first place.

“The carried interest loophole is a stain on the tax code,” Ackman said in a Thursday tweet.

While a billionaire hedge fund manager may seem like an unlikely backer of the Dems’ fight against tax loopholes, Ackman has actually been arguing for the closure of the carried interest loophole for a decade now.

But before jumping into the billionaire’s beef with carried interest, it’s best to define some key terms.

Cross border tax advice Carried interest: A ‘loophole’ or an entrepreneur’s best friend?

Private equity and hedge funds earn money in two key ways. First, they charge a base management fee on the total amount of money a client has invested. Second, they earn a share of the profits from their fund’s investments if they achieve a minimum return known as the hurdle rate. Any profits earned by managers above the hurdle rate are called carried interest.

The carried interest provision allows fund managers to pay a capital gains tax rate (roughly 20%) on these earnings, instead of the much higher regular income tax rate (37% for single filers’ taxable income above $539,900).

This tax treatment, or “loophole,” depending on who you ask, is supposed to incentivize money managers to earn better returns for their investors. But Ackman questioned this purported purpose on Friday in a Twitter thread.

“The daily activity of investment management does not need the additional incentive of lower carried interest taxation to drive behavior,” he said. “Put simply, there should be no difference in the tax rate on the management fee income investment managers receive compared to the incentive fees they receive as they are simply fees in various forms…They don’t need the extra boost from lower rates to motivate them to work better or harder for their clients. The fees are sufficient to motivate their behavior.”

Ackman isn’t the only big name on Wall Street that has spoken out against the carried interest loophole. Berkshire Hathaway CEO Warren Buffett has argued for closing the loophole for over a decade.

“If you believe in taxing people who earn income on their occupation, I think you should tax people on carried interest,” he said at a congressional hearing in 2010.

Still, proponents of the current carried interest tax treatment argue that changes to the tax code will hurt entrepreneurs.

“Increasing taxes on carried interest means many entrepreneurial firms and small businesses across sectors will not have access to the capital they need to compete, scale, innovate, and navigate challenging economic conditions,” the Small Business and Entrepreneurship Council said in a Friday statement. “This will only hurt local economies and workers, and more broadly undermine U.S. competitiveness.”

Drew Maloney, the CEO of the American Investment Council, also rebuked attempts to close the carried interest tax treatment in a Thursday statement.

“Over 74% of private equity investment went to small businesses last year,” he said. “As small-business owners face rising costs and our economy faces serious headwinds, Washington should not move forward with a new tax on the private capital that is helping local employers survive and grow.”

The Commercial Real Estate Development Association also argues that closing the carried interest will “disproportionately impact the real estate industry since real estate partnerships comprise a large number of partnerships and many use a carried interest component in structuring development ventures.”

And even Ackman noted on Friday that carried interest has value for entrepreneurs, allowing them to have favorable tax treatment as a sort of payment for the risks they take that can drive economic growth.

“This system has driven enormous job and wealth creation and is the biggest driver of our economy. It, therefore, needs to be preserved at all costs,” he wrote. “Giving favorable tax treatment for entrepreneurs who build businesses, develop real estate, drill for gas, sequester carbon, etc. creates powerful incentives that drive these high-risk activities and presents investment opportunities for passive investors who don’t have these capabilities.”

But when it comes to private equity and hedge fund managers, Ackman said the carried interest loophole doesn’t add any value.

“It does not help small businesses, pension funds, other investors in hedge funds or private equity, and everyone in the industry knows it. It is an embarrassment, and it should end now,” he said.

Sign up for the Fortune Features email list so you don’t miss our biggest features, exclusive interviews, and investigations.

This news is brought to you by IWTA. Founded in 2015 and located on Avenue of the Americas, in the heart of New York City, International Wealth Tax Advisors provides highly personalized, secure and private global tax, GILTI, FATCA, Foreign Trusts consulting and accounting to many IWTAS.COM clients worldwide, including: Singapore, China, Mexico, Ecuador, Peru, Brazil, Argentina, Saudi Arabia, Pakistan, Afghanistan, South Africa, United Kingdom, France, Spain, Switzerland, Australia and New Zealand.

” alt=”us totalization agreements Is your crypto exchange prepared to issue 1099-Bs? Here’s how to do it easily” data-src=”https://cryptoslate.com/wp-content/themes/cryptoslate-2020/imgresize/timthumb.php?src=https://cryptoslate.com/wp-content/uploads/2022/07/crypto-exchange-tax.jpg&w=70&h=37&q=75″ data-srcset=”https://cryptoslate.com/wp-content/themes/cryptoslate-2020/imgresize/timthumb.php?src=https://cryptoslate.com/wp-content/uploads/2022/07/crypto-exchange-tax.jpg&w=105&h=55&q=75 1.5x, https://cryptoslate.com/wp-content/themes/cryptoslate-2020/imgresize/timthumb.php?src=https://cryptoslate.com/wp-content/uploads/2022/07/crypto-exchange-tax.jpg&w=140&h=74&q=75 2x” />Is your crypto exchange prepared to issue 1099-Bs? Here’s how to do it easilyTrent Bigelow ·6 hours ago· 4 min read

In order to be prepared for this change, you need to know what exactly is coming quickly down the road for crypto exchanges and wallets, what kind of reporting will be required of you, and why it might not be a good idea to build those capabilities in-house.

Taxes are one of the few certainties in life, and big tax changes are coming for crypto exchanges and wallets very soon. Will you be ready for them?

While cryptocurrency owners have been required to report their crypto gains and losses on their income taxes for a few years now, crypto exchanges and wallets haven’t needed to provide information to the IRS on their customers and their transactions. But that’s all changing, as new federal regulations will require crypto exchanges and wallets to provide tax documents in the form of a 1099-B to their customers. And it’s not going to be an easy process.

In order to be prepared for this change, you need to know what exactly is coming quickly down the road for crypto exchanges and wallets, what kind of reporting will be required of you, and why it might not be a good idea to build those capabilities in-house.

Us totalization agreements What’s on the Horizon for Tax Reporting

Despite cryptocurrency’s intention to be decentralized, federal tax regulations have caught up to crypto owners, who must report their crypto holdings as property and pay any capital gains taxes associated with it. However, unlike brokerage or barter exchanges, crypto exchanges and wallets haven’t had to report customer information, transactions, and gains or losses to the IRS, and issue a form to customers for their own tax purpose.

However, that has changed with the Infrastructure Investment and Jobs Act, also known as the Infrastructure Bill, on November 15, 2021. The Bill expands required tax reporting for crypto transactions and starting in 2023, crypto exchanges and wallets will be required by law to generate and issue 1099-B forms — or something like it — to their customers, the Federal government, and each state that requires reporting. And with nearly 600 crypto exchanges out there — with the largest one running a $15.9 billion volume — there’s a lot of work ahead of them.

A 1099-B — like other 1099 forms — is used to report non-W2 income earned over $600 and are records of freelance or gig work, interest received, dividend payouts, and more. Even certain purchases using crypto coins can trigger a taxable event applying to the $600 threshold. A 1099-B form is specifically issued by brokerage firms and barter exchanges and contains a record of all transactions made, the instrument used, gains or losses, and more. The message here is clear: The IRS is viewing your exchange like a brokerage firm or barter exchange. And as such, you have to track and provide a record of all crypto transactions per customer made on your platform. You may also have to report on existing tax obligations like backup withholdings as well.

Because this is required by law, you don’t have an option to do nothing — or you can and face the penalty. You need to build out your capability to handle this massive amount of data collection and tracking, so that come next year. But how will you do that?

Us totalization agreements How to Prepare Your Exchange

Crypto exchanges and wallets need to prepare for this new tax regulation end-to-end, from collecting customer information to tracking and attributing transactions to generating a form that complies with the tax law. What kind of information does a typical 1099-B contain? You can find a customer’s name, address, and social security number — and SSNs require their own process to collect and verify before 1099-B issuance can begin. It also contains a list of every transaction made, including what was sold, the date sold, the quantity, the gain or loss, and other important information.

It’s a lot of data to track and a lot of reporting to get correct. Your first thought may be to build these capabilities in-house, but you’ll be facing a number of hurdles to doing so, like:

Compliance: There are a number of challenges to building in-house. The first is compliance and making sure that how you’re gathering and reporting information adheres to this new tax law. And you can be sure that the IRS will keep an eye on crypto exchanges and wallets to ensure they’re getting it right.

Speed: Another challenge will be the speed at which you can design, develop, and deploy these new capabilities — especially when they need to be ready by the end of the year. Do you have the resources and budget to immediately turn your attention to solving this problem?

Cost: Cost is another challenge if you build in-house. Consider the research, design, sourcing, development, testing, and maintenance costs of building, running, and maintaining the backend infrastructure of this capability. Does your exchange have the engineering resources to prioritize this as well?

Maintenance: Finally, are you prepared to commit to the ongoing work to run this tax process year after year and maintain the underlying infrastructure? Who will be making the software updates to keep up with evolving tax laws? What team will own this?

Us totalization agreements Use Custom APIs

You don’t have to build your solution yourself. The best approach to get you up and running quickly and easily is to use APIs to track and generate your 1099-Bs. Instead of building all those capabilities in-house, APIs will integrate with your system and easily pull all that data to generate the forms you need. Plus, custom-built APIs from a knowledgeable vendor will ensure that you’re not only keeping compliant with tax law but that you’re keeping up with any changes and ongoing maintenance of the API. Ultimately, going with API integration will save you time, money, and resources and prepare you for the new laws to take effect.

Us totalization agreements Tax Changes for Crypto Exchanges

An old adage says that there are only two things certain in life, and one of them is taxes. Crypto exchanges and wallets are facing an inevitable future of compliance when it comes to transaction reporting to the IRS — and possibly even more expanded reporting, including the taxability of staking. However, another old adage says that a stitch in time saves nine, so if crypto exchanges and wallets begin to build out their capabilities today, they won’t be scrambling when the IRS comes calling.

Guest post by Trent Bigelow from Abound

Trent Bigelow is co-founder and CEO of Abound. The company’s APIs enable those serving or paying independent workers (1099ers) to quickly and effortlessly embed benefits into their products, automatically setting aside enough to cover taxes, retirement, healthcare, insurance, PTO, and more. Trent leads the company’s strategy to increase wealth and wellness for 68 million self-employed Americans, unlocking access to independent benefits in an easy, affordable, and compliant way that works for everyone.

This news is brought to you by IWTA. Founded in 2015 and located on Avenue of the Americas, in the heart of New York City, International Wealth Tax Advisors provides highly personalized, secure and private global tax, GILTI, FATCA, Foreign Trusts consulting and accounting to many IWTAS.COM clients worldwide, including: Singapore, China, Mexico, Ecuador, Peru, Brazil, Argentina, Saudi Arabia, Pakistan, Afghanistan, South Africa, United Kingdom, France, Spain, Switzerland, Australia and New Zealand.

US Secretary of Treasury Janet Yellen arrives at the meeting room during the G20 Finance Ministers Meeting in Nusa Dua, Bali, July 15, 2022. — Reuters pic

Follow us on Instagram, subscribe to our Telegram channel and browser alerts for the latest news you need to know.

Saturday, 16 Jul 2022 11:53 PM MYT

NUSA DUA, Indonesia, July 16 — The United States will look for every opportunity to move ahead and enact a global minimum corporate tax agreement despite the opposition of a key Democratic senator, Joe Manchin, to raising corporate taxes, US Treasury Secretary Janet Yellen said.

Yellen told reporters today that finance officials from the Group of 20 major economies reached strong consensus about many issues, including the need to address a worsening food security crisis, despite differences over Russia’s war in Ukraine that prevented the leaders from issuing a joint statement.

Manchin, who holds the pivotal vote in the evenly divided Senate, this week said he would not support a Democratic proposal for new climate change spending and higher taxes for corporations and wealthier Americans.

His opposition could imperil passage of legislation that would commit the United States to a 15 per cent global minimum corporate tax, a key part of an agreement that Yellen helped negotiate with nearly 140 countries last year.

“We are very committed to moving ahead with this. This is a truly important global initiative,” she said on the second day of a two-day G20 meeting in Bali. “I can tell you that we will continue to look for every possible opportunity that we have to move this forward.”

She said the United States had a strong incentive to move forward because as other countries enacted the tax agreement, they would be taxing the foreign profits of US companies, while the United States would be leaving “that tax revenue on the table rather than capturing it ourselves.”

Yellen said it was important that Manchin did signal support for legislation to reduce prescription drug prices for seniors and extending subsidies that help keep health insurance costs lower.

On his opposition to climate change provisions, Yellen said Treasury would support US President Joe Biden’s plans to use executive action, and would continue initiatives under the Financial Stability Oversight Council to evaluate the risks posed by climate change to financial institutions.

She also addressed the recent strong appreciation of the US dollar and said it was due to strong economic growth, moves by the Fed to raise interest rates, and capital inflows.

“The US position is that we believe in market-determined exchange rates” and it is very rarely appropriate to intervene, Yellen said, adding “I do not see this as one of these occasions.” — Reuters

This news is brought to you by IWTA. Founded in 2015 and located on Avenue of the Americas, in the heart of New York City, International Wealth Tax Advisors provides highly personalized, secure and private global tax, GILTI, FATCA, Foreign Trusts consulting and accounting to many IWTAS.COM clients worldwide, including: Singapore, China, Mexico, Ecuador, Peru, Brazil, Argentina, Saudi Arabia, Pakistan, Afghanistan, South Africa, United Kingdom, France, Spain, Switzerland, Australia and New Zealand.

What Are Three Essential Tax Laws Foreign Owners of U.S. Real Estate Need to Know?

Jack Brister

Founder, International Wealth Tax Advisors

Jack Brister, Founder of International Wealth Tax Advisors, is a noted international tax expert, with over 25 years of experience. Jack specializes in U.S. tax planning and compliance for non-U.S. families with international wealth and asset protection structures.

Jack is a frequent featured speaker at numerous international financial conferences and has been named a Citywealth Top 100 U.S. Wealth Advisor.

Contact IWTA

To schedule an introductory phone conference with IWTA founder Jack Brister simply clickhere. Email IWTA atbloginquiries@iwtas.com Or call the IWTA New York City office at 212-256-1142

What Do Foreign Owners of U.S. Real Estate Need to Know?

Real estate is a popular investment choice for non-U.S. investors, but foreign investors need to take careful considerations when looking to invest. These considerations include income, business structure and the property value, to name a few. With no one-size-fits-all, investors need proper planning and advice to avoid possible tax and penalty complications.

What is the U.S. Estate Tax Exemption?

While U.S. citizens andpersons who are deemed to be domiciledcan enjoy an estate tax exemption in 2022 of $12,060,000, that figure does not apply to nonresident aliens. The exemption amount for a nonresident alien decedent is actually only $60,000, and any amount that exceeds that figure is subject to estate tax that ranges anywhere from 26% – 40% . The estate tax exemption applies to all assets, not just real estate. Real estate property falls under the blanket estate tax exemption if the property is an asset in a decedent’s estate.

What Taxes are Nonresident Aliens Responsible For?

If a business entity or revocable trust holds U.S. properties they may be required to file annual federal and possibly state tax returns.

Lessors of U.S. property or recipients of rental income of that property must file a Form 1040-NR U.S. Nonresident Income Tax Return for the income.

State and city taxes may also be levied.

Reports may also need to be filed with the Financial Crimes Enforcement NEtwork (FinCEN) or the IRS, including the FBAR and Form 5472.

Failure to file may result in fines, and if not resolved, the property can be seized or sold at auction, and nonresident aliens with a federal tax lien can have their information shared with the Department of Homeland Security.

Can Visits to the U.S. Impact Taxes?

Visits exceeding 183 days in a given year or over a three-year period (see below example) can impact residency status for tax purposes, which would subject an individual to tax on worldwide income and foreign financial assets and accounts as well as additional filings for any interest in a foreign business and bank accounts. The United States calculates this by using thesubstantial presence test.

For example:

Year

# of Days in US

Calculation

Current

85

85 x 1 = 85 days

Prior

100

100 x ⅓ = 33 days

Two Years Prior

120

120 x ⅙ = 20

Total Days in the US

138

The above individual would not qualify as a resident under the substantial presence test.

To avoid the substantial presence test, individuals should limit visits to less than 120 days of presence each calendar year. There are also other ways to avoid being considered a U.S. resident for tax purposes, including job roles (certain visas), professional athletes temporarily competing in a charitable event, or if time was spent stateside due to a medical condition occurring while visiting the U.S. Additionally there are exemptions for closer connections. Individuals that do meet the exemption should file IRS Form 8843.

As foreign individuals look to invest, it is helpful to know the intricacies of the U.S. and foreign tax system. Foreign investors holding real estate properties or other assets in the U.S. are encouraged to seek the advice of a tax consulting and accounting firm that specializes in the intricacies of U.S. tax reporting as it applies to international investors and trust holders.

Jack Brister, Founder of International Wealth Tax Advisors, is a noted international tax expert, with over 25 years of experience. Jack specializes in U.S. tax planning and compliance for non-U.S. families with international wealth and asset protection structures.

Jack is a frequent featured speaker at numerous international financial conferences and has been named a Citywealth Top 100 U.S. Wealth Advisor.

Contact IWTA

To schedule an introductory phone conference with IWTA founder Jack Brister simply clickhere. Email IWTA atbloginquiries@iwtas.com Or call the IWTA New York City office at 212-256-1142

TIGTA Highlights the IRS’ FATCA Enforcement Woes

In the first 12 years of the U.S. Foreign Account Tax Compliance Act, the IRS has spent nearly $600 million on enforcement but has only managed to collect $14 million in penalties in return. This poor performance indicates that the agency strongly needs to revise its enforcement strategy according to a recent audit report by the Treasury Inspector General for Tax Administration.

Initially, the IRS had big compliance plans for FATCA and published a sprawling compliance roadmap addressing several aspects of FATCA. But years of budget constraints and other personnel resource issues led the IRS to shrink those plans to two compliance campaigns, which are handled by the IRS’ Large Business & International division.

The first campaign, Campaign 896, focuses on offshore private banking and U.S. taxpayers who have either underreported or failed to report their foreign assets on Form 8938. According to the IRS, over 330,000 taxpayers with foreign accounts exceeding $50,000 failed to file the form between 2016 and 2019. This means the government could collect at least $3.3 billion in penalties from the group, if each taxpayer pays the minimum FATCA penalty, which is $10,000.

The second campaign, Campaign 975, focuses on the accuracy of taxpayers’ FATCA filings, but the IRS has only been able to review one tax year — 2016 — leaving the agency far behind its goals.

All of this means that the IRS has a lot of work to do in monitoring FATCA and ensuring taxpayers are complying with the law. In anaudit reportpublished April 7, the Treasury Inspector General for Tax Administration described some of the IRS’ progress and setbacks with FATCA compliance. TIGTA conducted the audit to evaluate how the IRS has been using the information it gathers under FATCA to improve taxpayer compliance.

The most important takeaway is that the IRS is planning to increase its audits and reviews of U.S. foreign account holders, meaning that taxpayers with such accounts should prepare for increased scrutiny. If they have any unreported accounts, they should also evaluatevoluntary disclosure and other optionsto potentially minimize any penalties from the government.

THE ABCs of FATCA

The U.S. government created FATCA to ensure transparency of U.S. taxpayers’ offshore financial accounts and combat tax evasion. Under the law, taxpayers with a certain threshold of foreign financial assets. must fileForm 8938, Statement of Specified Foreign Financial Assets. The thresholds, which start at $50,000 and top out at $600,000, depend on the taxpayer’s marital status and whether they live in the U.S. or abroad. Foreign financial institutions also have reporting obligations. Those with U.S. taxpayer assets are required to share information about those clients’ financial accounts with the IRS. Institutions that fail to do soare subject to a 30 percent withholding rate on their U.S. source payments.

Updating Procedures and Tightening the Reins

The IRS has spent a lot of money on FATCA compliance — over $573 million dollars — yet it has only collected a small fraction of that amount — $14 million — in FATCA penalties. In light of this lackluster performance, TIGTA made six recommendations to the IRS, some of which the IRS said it has already implemented, and others it is currently working on.

The first TIGTA recommendation is that the LB&I (Large Business and International) Division needs to tighten its surveillance of taxpayers who underreport their foreign assets and step up its compliance activity for that group, including levying penalty assessments and conducting examinations on taxpayers who consistently underreport. The IRS said it has already implemented that recommendation. For a list of currently published LB&I campaignsclick here.

The second recommendation is that the IRS should establish procedures for identifying taxpayers who fail to file Form 8938 and particularly focus on examinations or penalty assessments for that group. The IRS said it already has a filter that identifies potential non-filers. Importantly for taxpayers, the IRS revealed that it is currently conducting civil and criminal examinations on non-filing taxpayers and is considering penalties in examinations, when they are appropriate.

The third recommendation is that the LB&I Division needs to ensure that foreign financial institutions are also complying with FATCA, and should think about expanding the scope of Campaign 975 to address taxpayers and foreign financial institutions alike. The IRS said it agreed and that Campaign 975 is doing just that. According to the IRS, the agency has already reviewed about 4,000 foreign financial institutions and flagged potential noncompliance by 34 institutions. Although this is a good development, the seemingly small level of noncompliance suggests that the IRS should not devote extensive resources to this, and might be better served by focusing more heavily on individual taxpayers.

But TIGTA and the IRS disagreed over the auditor’s fourth suggestion. The IRS requires foreign financial institutions to include taxpayers’ taxpayer identification numbers on their FATCA report (Form 8966), but between 2017 and 2019 the IRS exempted some institutions, allowing more time to comply with the requirement. TIGTA believes the IRS should now issue a notice to foreign countries that their financial institutions must collect and provide the taxpayer identification numbers of U.S. individuals owning a foreign bank account.

The IRS believes this is not necessary because it issued a notice about this in 2017 (Article 2, Model 1A Reciprocal IGA;Notice 2017-46). TIGTA pushed back on this and wrote that the IRS should not assume that foreign financial institutions are aware of the 2017 notice and know what to do. They pointed out that less than half of the Form 8966s filed between tax years 2016 and 2019 had a valid TIN. The majority had an invalid TIN or completely lacked one. If the IRS does implement TIGTA’s recommendation, this could bring greater transparency to the agency’s investigations and compliance campaigns.

The fifth recommendation is that the IRS should establish goals, milestones, and timelines for FATCA campaigns in order to determine whether the campaigns are effective in meeting their objectives and affecting tax compliance. The IRS agreed with this and pledged to refine their metrics with respect to goals, milestones, and timelines.

Lastly, TIGTA recommended that the IRS should create an information sharing program that would allow the agency’s Small Business/Self-Employed division to access FATCA data and use it for examinations and collection actions. The IRS said it has implemented that recommendation.

A Tighter Leash for FATCA Compliance

The fact that the IRS already has implemented some of TIGTA’s recommendations demonstrates the agency’s seriousness about FATCA and ensuring that taxpayers and foreign financial institutions comply with the law. TIGTA’s report shows that the IRS’ FATCA issues are two-fold: first, the agency needs additional resources to oversee FATCA, but it also needs to better allocate the resources it does have. Considering that the Biden administration recentlyincreased the IRS’ budget, a tighter leash for FATCA laggards and new FATCA-related compliance campaigns could be right around the corner.

Sen. Elizabeth Warren is leading fellow Democrats in renewing a push for the IRS to create its own free tax-filing services and move away from its current private partnership, whose services only a slim portion of taxpayers use.

Warren, D-Mass., put forward a bill that would mandate the IRS create its own free, online program for preparing and filing tax returns and expand taxpayers’ access to their own tax-related data held by the agency. California Democrats Brad Sherman and Katie Porter led introduction of a House version of the measure.

The legislation would direct the IRS to create software that would allow any taxpayer to prepare and file their individual income tax return beginning in tax year 2023. The agency would also have to allow taxpayers with fairly straightforward returns — those who don’t take any above-the-line deductions, itemize their deductions or receive income as a sole proprietor of business, for instance — to elect that Treasury prepares their tax return beginning in the 2023 tax year.

The IRS would have to create a program for taxpayers to securely download third-party-provided return information and IRS-held data related to their individual tax bills.

The bill would require a program by March 1, 2023, allowing taxpayers who don’t have to file tax returns to claim refundable tax credits. The provision aims to expand a sign-up tool for the child tax credit to nonfilers who can access other tax benefits like the earned income tax credit, which is open to low-income workers.

The measure would also bar the Treasury secretary from entering into any new agreements that would restrict the federal government’s right to provide services or software for preparing and filing taxes.

A fact sheet from the bill’s sponsors points to problems with the IRS Free File program, which currently aims to offer free tax preparation to 70 percent of taxpayers by partnering with private tax preparing firms. The lawmakers argued that program is underused, often confuses taxpayers into paying for services and fails to adequately protect taxpayer data. In the last two years, major online tax platforms H&R Block and Intuit’s TurboTax withdrew from the program.

Only 2.8 percent of all individual tax returns filed in fiscal 2021 were submitted through the Free File program, according to IRS data.

The bill picked up co-sponsors since its last introduction in 2019 and now has 22 Democratic senators signed on.

Warren has sought to tie the issue to Democrats’ push for a budget reconciliation bill. Senate Majority Leader Charles E. Schumer, D-N.Y., and Sen. Joe Manchin III, D-W.Va., are in talks in the hopes of agreeing to a package broadly including pieces to lower prescription drug costs, incentivize clean energy production and increase taxes on the wealthy and corporations.

The latest Senate version of the legislation included about $80 billion over a decade for the IRS largely intended to boost its ability to go after uncollected taxes and raise federal revenue in the process. It also included $15 million for the IRS to study the feasibility of creating a free, direct online tax return system.

When Treasury Secretary Janet L. Yellen appeared before the Finance Committee in June, Warren pressed her for a commitment the IRS will go farther and build its own free filing system if Congress delivers the $80 billion cash infusion.

Yellen pointed to more pressing priorities like working through a massive backlog of tax returns, but agreed the IRS would take up the issue when it’s “adequately resourced.”

This news is brought to you by IWTA. Founded in 2015 and located on Avenue of the Americas, in the heart of New York City, International Wealth Tax Advisors provides highly personalized, secure and private global tax, GILTI, FATCA, Foreign Trusts consulting and accounting to many IWTAS.COM clients worldwide, including: Singapore, China, Mexico, Ecuador, Peru, Brazil, Argentina, Saudi Arabia, Pakistan, Afghanistan, South Africa, United Kingdom, France, Spain, Switzerland, Australia and New Zealand.

According to recent reports, the HMRC are warming up to cracking down on over 300 Premier League stars, 31 clubs, and 91 agents for tax avoidance.

The HMRC are said to be motivated to take action in recent times based on the tactics clubs are deploying in recent times to evade tax.

As it is seen to be customary, endorsement royalties linked to image rights are expected to be paid to the firm the player is set up with, where the firm will end up being taxed.

However, it has become public knowledge that Premier League clubs especially are now paying all directly to the player to avoid taxation.

The Sun further reports that there seem to be some inconsistencies related to the commission clubs are paying to agents, which are mandatory to be taxed.

Newcastle are reported to be at the forefront of this issue as they are currently arm-wrestling themselves out of the £5 million tax demand relating to transfers.

A partner at the accountancy group UHY Hacker Young, Elliot Boss told The Sun, “The Football Compliance Project linking up with HMRC’s elite fraud unit means the tax authority is very concerned about the significant amounts of unpaid tax in the sport, “

“HMRC sees football as an industry where millions of pounds in tax can very easily go unpaid. It is determined not to let that happen.”

HMRC Taxation Avoidance Reports Last Year

As of last year, it was reported that about 93 players, nine clubs and 23 were in the thick of things as regards being investigated for tax avoidance – Which gives perspective on how worrisome this year’s figure is.

In an exclusive with the Sun last year, Buss pointed out that:

“HMRC sees the football industry as an area where there is a great deal of unpaid tax owed by high earners. HMRC has identified £55.6m in unpaid tax from the football industry.

“Targeting agents’ fees is a signal they think this is an area where too much tax is underpaid… it is understandable the likes of Marcus Rashford or Harry Kane would utilize a company to sell their ‘image’. But players with near to no brand recognition use image rights to avoid paying tax.”

This news is brought to you by IWTA. Founded in 2015 and located on Avenue of the Americas, in the heart of New York City, International Wealth Tax Advisors provides highly personalized, secure and private global tax, GILTI, FATCA, Foreign Trusts consulting and accounting to many IWTAS.COM clients worldwide, including: Singapore, China, Mexico, Ecuador, Peru, Brazil, Argentina, Saudi Arabia, Pakistan, Afghanistan, South Africa, United Kingdom, France, Spain, Switzerland, Australia and New Zealand.

Jack Brister, Founder of International Wealth Tax Advisors, is a noted international tax expert, with over 25 years of experience. Jack specializes in U.S. tax planning and compliance for non-U.S. families with international wealth and asset protection structures.

Jack is a frequent featured speaker at numerous international financial conferences and has been named a Citywealth Top 100 U.S. Wealth Advisor.

Contact IWTA

To schedule an introductory phone conference with IWTA founder Jack Brister simply clickhere. Email IWTA atbloginquiries@iwtas.com Or call the IWTA New York City office at 212-256-1142

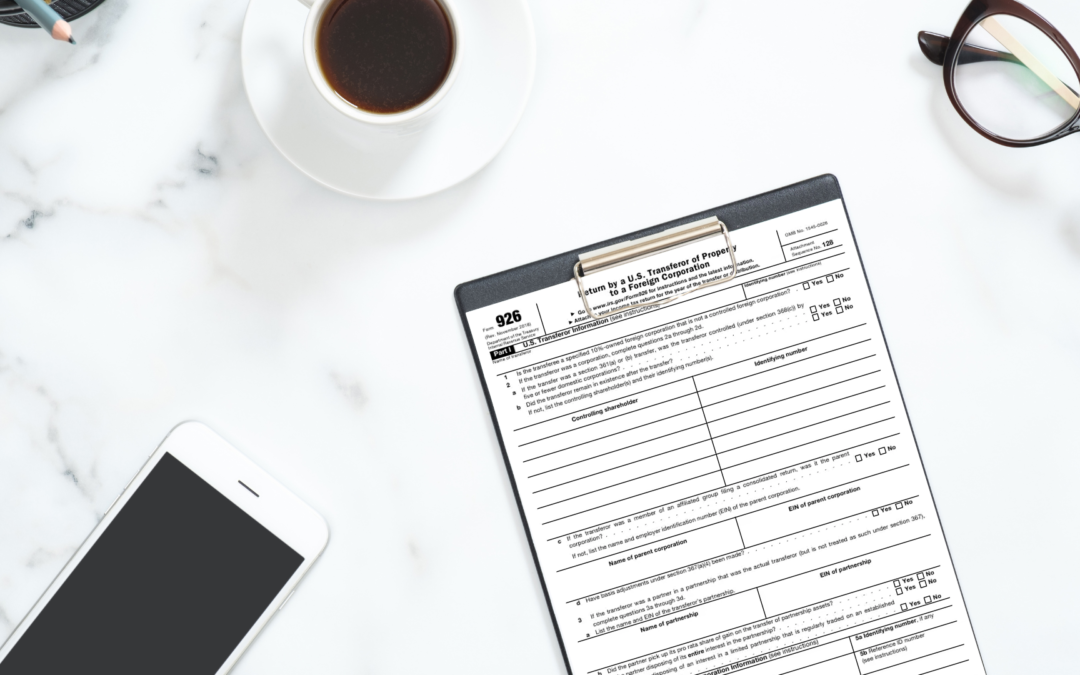

The Cost of Non-Compliance With IRS Form 926

The 16th amendment of the U.S. Constitution empowers Congress to collect taxes from U.S. persons from whatever source, with no limitations on the collections of taxes or worldwide income. All United States tax laws and regulations apply to every U.S. Person whether he/she is working in the United States or in a foreign country and entities formed under U.S. law. The IRS takes this opportunity increasingly seriously, and taxpayers need to do the same.

IRS Form 926 is the form U.S. citizens and entities including estates and trusts must file to report certain exchanges or transfers of property to a foreign corporation. This would include transfers of cash over $100,000 to a foreign corporation, or situations in which the transfer of cash resulted in owning more than 10% of the foreign corporation’s stock. This reporting requirement applies to outbound transfers of both tangible and intangible property.

The primary purpose of Form 926 is to ensure that taxable gain is recognized and tax is paid. The reason for the complexity is the attempt of U.S. tax law to formalize distinction between legitimate business operations outside the U.S. and transactions considered to avoid tax.

It is also designed to equalize the taxation between transactions within the U.S. and outside the U.S. In that way there are no significant advantages to transactions and operations outside the U.S..

Form 926 must be complete, accurate, and filed with the taxpayer’s income tax return by the due date of the return (including extensions).

Penalties are Severe and Limitless

In an attempt to prevent taxpayers from hiding assets offshore or earning unreported income overseas, the IRS has recently begun increasingly aggressive enforcement of cross-border corporate reorganizations, divisions, and liquidations.

The rules surrounding Form 926 are extremely complex, therefore, correct filing of the form requires a high level of scrutiny. There are literally dozens of stipulations and technical details that must be followed.

The failure to file, fully meet the filing requirements, or misrepresentation of assets can result in the levying of substantial penalties. For example, the statute of limitations doesn’t end until three years after the date Form 926 is filed. However, if the form was never filed to begin with, the statute of limitations clock hasn’t started yet. This means the IRS could assess a penalty at any time, even 20 years after the missed mandatory deadline.

Returns that are filed but that are not substantially complete and accurate are considered “un-filed” and may result in penalty assessments. Criminal penalties may apply to U.S. and foreign taxpayers who willfully fail to file a return (IRC 7203) or file a false or fraudulent return (IRC 7206 and IRC 7207).

Certain international information returns are also considered un-filed if the taxpayer does not provide required information when requested by the IRS, and penalties may be assessed even if the required return has been submitted.

If a taxpayer under-reports on Form 926 and that leads to a tax underpayment, they can receive a 40% penalty. Sometimes a tax penalty may be avoided if the filer can show that the misrepresentation was due to reasonable cause and they acted in good faith – but don’t count on it.

IRS: Ignorance of the Requirements is No Excuse

The IRS maintains that taxpayers who conduct business or transactions offshore or in foreign countries have a responsibility to exercise ordinary business care and prudence in determining their filing obligations and other requirements. The IRS’s position is that lack of information or misinformation is not grounds for dismissal of taxes and penalties; therefore, it’s incumbent on the individual taxpayer or entity to learn and comply with the rules related to Form 926. Engaging the services of a qualified tax consultant-CPA and law firm specializing in international tax and business transactions will ensure compliance is met.

For more information on U.S. tax rules as they apply to U.S. taxpayers that are foreign investors or hold foreign assets, refer to the following articles on the International Wealth Tax Advisors website:

India’s government on July 1 implemented a 1% tax deducted at the source (TDS) on every cryptocurrency trade over 10,000 Indian rupees, or about $127. The law has only been in place a few days, but there’s already been a chilling effect on Indian digital asset marketplaces.

The levy is an addition to the 30% tax on all crypto-based incomes that began on April 1, which is double India’s 15% capital gains tax on short-term gains for traditional equities and shares.

The increasing taxation could serve as a further roadblock for citizens looking to trade crypto as the potential for financial gains dwindles.

This news is brought to you by IWTA. Founded in 2015 and located on Avenue of the Americas, in the heart of New York City, International Wealth Tax Advisors provides highly personalized, secure and private global tax, GILTI, FATCA, Foreign Trusts consulting and accounting to many IWTAS.COM clients worldwide, including: Singapore, China, Mexico, Ecuador, Peru, Brazil, Argentina, Saudi Arabia, Pakistan, Afghanistan, South Africa, United Kingdom, France, Spain, Switzerland, Australia and New Zealand.

The Conservative Party and the NDP are calling on Canada Revenue Agency Commissioner Bob Hamilton to testify before a Parliamentary committee after a massive disclosure of sensitive internal documents revealed numerous allegations of wrongdoing at a CRA division responsible for ensuring multinational companies pay appropriate levels of Canadian tax.

The documents suggest that at least some of the tension in the division was owing to a disagreement over the agency’s handling of a specific multimillion-dollar tax agreement reached with a multinational company. The identity of the company in question is repeatedly redacted in the documents.

Some division staff disagreed with the tax agreement because they saw it as a “sweetheart” deal for the company and opposed the way it was approved, the records show. Staff who felt the division was under inappropriate pressure to approve the agreement filed internal complaints.

The documents relate to turmoil inside the CRA’s Competent Authority Services Division, which is part of the agency’s international and large business directorate. The CASD works with international companies that operate in Canada to determine their Canadian tax obligations.

The now-former head of the division, Donna O’Connor, breached hiring rules and failed to set an appropriate leadership tone, according to the findings in a December, 2019, report produced by the CRA’s internal affairs and fraud control division and filed as part of the court case. The CRA report says Ms. O’Connor told a CRA investigator that her “division was corrupt,” but did not elaborate. Ms. O’Connor also said she was trying to clean up bad practices, according to the report.

During a Monday meeting of the House of Commons Finance committee, Conservative MP Dan Albas provided notice of a motion calling on Mr. Hamilton to appear and explain the issues raised in the documents. The committee could vote on the matter as soon as Tuesday.

Mr. Albas told The Globe and Mail after the meeting that the Liberal government frequently boasts it is working hard on the world stage to ensure large companies pay their fair share of tax. But he noted the documents suggest some within the CRA disagree with how such files are handled.

“That’s one of the reasons why I’d like to have the commissioner come before committee, so that he can lay out his case as to what is occurring at CRA under his watch,” Mr. Albas said.

NDP finance critic Daniel Blaikie said he will support the Conservative motion calling for Mr. Hamilton to appear. He noted the CRA has long been accused by critics of doing a poor job of enforcing tax rules for wealthy people and large corporations.

“And so when you couple that with these stories about a broken culture that even people within the CRA are calling corrupt, it is very concerning,” he said.

Liberal and Bloc Québécois MPs did not say Monday whether they would vote for the motion, which would require the support of a majority of MPs on the committee for it to go ahead.

CRA spokesperson Etienne Biram said in a statement Monday that the allegations related to the specific tax deal were reviewed by the CRA’s internal fraud division and a third party expert in tax law.

“While complaints in the Federal Court documents claim a ‘sweetheart deal’ was struck in 2019, the investigation determined that the terms of the [agreement] were in fact favourable to the CRA and did not provide any form of preferential treatment,” Mr. Biram said in an e-mail. He also said allegations that the deal was granted with no analysis and that employees were forced from their positions were all deemed to be unfounded.

Mr. Biram said the CRA takes allegations of misconduct seriously, but he added that it is difficult for the agency to respond to allegations that are before the Federal Court. He also noted that the Federal Court case is about two other allegations that are not related to the tax deal.

The Federal Court case began in September, 2021, when two CRA employees asked the court to review a decision by Public Sector Integrity Commissioner Joe Friday to stop investigating their allegations of wrongdoing at the CRA. The commissioner explained in letters to the employees that he felt his office did not need to investigate because the agency was already dealing with the matter.

Documents related to the commissioner’s investigation, which began in 2020, were submitted to the court, making them publicly available.

The commissioner’s office told The Globe last week that it was approached on April 12 by the Attorney-General, on behalf of the CRA, and made aware that some of the documents contain sensitive information. On April 19, the commissioner’s office wrote to the Federal Court, saying it intended to replace its court filings with new versions of the documents that will redact “irrelevant” third-party information, including the names of people who made allegations and the names of those against whom the allegations were made.

The Conservative Party asked Privacy Commissioner Daniel Therrien to launch an investigation into the release of “sensitive whistle-blower information” after the website Blacklock’s Reporter wrote about the case last month.

The court documents show the Integrity Commissioner’s office investigated a wide range of allegations put forward by the two CRA employees and determined that some warranted further review and others did not.

In a July 21, 2020 letter from Mr. Friday to one of the employees, the commissioner said he would be investigating some but not all of the allegations. Mr. Friday agreed to investigate concerns over travel expenses in the division and the possibility that it had a “toxic” work environment.

But Mr. Friday’s letter said he would not be investigating an allegation related to the specific tax deal, in part because his office is not authorized to review information that is subject to solicitor-client privilege.

For subscribers: Get exclusive political news and analysis by signing up for the Politics Briefing.

This news is brought to you by IWTA. Founded in 2015 and located on Avenue of the Americas, in the heart of New York City, International Wealth Tax Advisors provides highly personalized, secure and private global tax, GILTI, FATCA, Foreign Trusts consulting and accounting to many IWTAS.COM clients worldwide, including: Singapore, China, Mexico, Ecuador, Peru, Brazil, Argentina, Saudi Arabia, Pakistan, Afghanistan, South Africa, United Kingdom, France, Spain, Switzerland, Australia and New Zealand.

WARSAW — Treasury Secretary Janet L. Yellen arrived in Europe this week to join U.S. allies in confronting multiple threats to the world economy: Russia’s war in Ukraine, soaring inflation and food shortages.

But one of Ms. Yellen’s first orders of business during a stop in Poland will be trying to get the global tax deal that she brokered last year back on track after months of fledgling deliberations about how to enact it. The two-pronged pact among more than 130 countries that was reached last October aimed to eliminate corporate tax havens by enacting a 15 percent global minimum tax. It would also shift taxing rights among countries so that corporations pay taxes based on where their goods and services are sold rather than where their headquarters are.

Turning the agreement into a reality is proving to be a steep challenge.

The European Union has already delayed its timeline for putting the tax changes in place by a year and progress has been halted over objections by Poland, which last month vetoed a plan to enact the new tax rate by the end of next year. Despite initially signing on to the deal, Poland has voiced reservations, including whether the minimum tax will actually prevent big tech companies from seeking out lower-tax jurisdictions. Polish officials have also expressed concern that the two parts of the tax agreement are moving ahead at different paces, as well as trepidation about the impact that raising its tax rate will have on its economy at a time when the country is absorbing waves of Ukrainian refugees.

In meetings in Warsaw on Monday, Ms. Yellen pressed top Polish officials to let the process move ahead, making clear that the tax deal continues to be a priority of the United States. She is meeting with Poland’s prime minister, Mateusz Morawiecki, and the finance minister, Magdalena Rzeczkowska.

According to the Treasury Department, Ms Yellen told Mr. Morawiecki that international tax reform and the global minimum tax would raise crucial revenues to benefit the citizens of both Poland and the United States.

The meetings come at the beginning of a weeklong trip that also includes stops in Brussels and Bonn, Germany, which is hosting the Group of 7 finance ministers’ summit. Ms. Yellen will be focusing on coordinating sanctions against Russia with European allies and addressing growing concerns about how disruptions to energy and food supplies could affect the global economy.

The tax agreement has been one of Ms. Yellen’s top priories as Treasury secretary. Gaining Poland’s support is critical because the European Union requires consensus among its member states to enact the tax changes.

“I think the reality of turning a political commitment into binding domestic legislation is a lot more complex,” said Manal Corwin, a Treasury official in the Obama administration who now heads the Washington national tax practice at KPMG. “The E.U. has moved and gotten over most of the objections, but they still have Poland and it’s not clear whether they’re going to be able to get the last vote.”

With President Emmanuel Macron of France heading the European Union’s rotating presidency until June, his administration was eager to get a deal implemented. But at a meeting of European finance ministers in early April, Poland became the sole holdout, saying there were no ironclad guarantees that big multinational companies wouldn’t still be able to take advantage of low-tax jurisdictions if the two parts of the agreement did not move ahead in tandem, undercutting the global effort to avoid a race to the bottom when it comes to corporate taxation.

Poland’s stance was sharply criticized by European officials, particularly France, whose finance minister, Bruno Le Maire, suggested that Warsaw was instead holding up a final accord in retaliation for a Europe-wide political dispute. Poland has threatened to veto measures requiring unanimous E.U. votes because of an earlier decision by Brussels to block pandemic recovery funds for Poland.

The European Union had refused to disburse billions in aid to Poland since late last year, citing separate concerns over Warsaw’s interference with the independence of its judicial system. Last week, on the eve of Ms. Yellen’s visit to Poland, the European Commission came up with an 11th-hour deal unlocking 36 billion euros in pandemic recovery funds for Poland, which pledged to meet certain milestones such as judiciary and economic reforms, in return for the money.

Negotiators from around the world have been working for months to resolve technical details of the agreement, such as what kinds of income would be subject to the new taxes and how the deal would be enforced. Failure to finalize the agreement would likely mean the further proliferation of the digital services taxes that European countries have imposed on American technology giants, much to the dismay of those firms and the Biden administration, which has threatened to impose tariffs on nations that adopt their own levies.

“It’s fluid, it’s moving, it’s a moving target,” Pascal Saint-Amans, the director of the center for tax policy and administration at the Organization for Economic Cooperation and Development, said of the negotiations at the D.C. Bar’s annual tax conference this month. “There is an extremely ambitious timeline.”

Countries like Ireland, with a historically low corporate tax rate, have been wary of increasing their rates if others do not follow suit, so it has been important to ensure that there is a common understanding of the new tax rules to avoid opening the door to new loopholes.

“The idea of having multiple countries put the same rules in place is a new concept in tax,” said Barbara Angus, the global tax policy leader at Ernst & Young and a former chief tax counsel on the House Ways and Means Committee. She added that it was important to have a multilateral forum so countries could agree on how to interpret and apply the levies.

Yet, while Ms. Yellen is pushing foreign nations to adopt the tax agreement, it remains unclear whether the United States will be able to pass its own legislation to come into compliance.

An earlier effort by House Democrats to adopt a tax plan that would satisfy terms of the agreement fell apart in the Senate, where Democrats continue to disagree over the scope and cost of a tax and spending bill that President Biden has proposed.

Republicans in Congress have made clear that they are unlikely to support any agreement that the Biden administration has brokered and called on the Treasury Department to consult with them before trying to move ahead.

“As it is, there’s very little chance of a global minimum tax agreement — there is already resistance to approval at the E.U., which should be the easiest part of these discussions, and it will only get harder going forward,” said Representative Kevin Brady of Texas, the top Republican on the House Ways and Means Committee. “Meanwhile, here in the U.S., there’s little political support for an agreement that makes the U.S. less competitive and takes a big bite out of our tax base.”

Ms. Yellen is expected to convey to her counterparts this week that the agreement is still a priority for the Biden administration and that she hopes that the United States can make the tax changes needed to comply with the agreement in a small spending package later this year, according to a person familiar with the negotiations.

This news is brought to you by IWTA. Founded in 2015 and located on Avenue of the Americas, in the heart of New York City, International Wealth Tax Advisors provides highly personalized, secure and private global tax, GILTI, FATCA, Foreign Trusts consulting and accounting to many IWTAS.COM clients worldwide, including: Singapore, China, Mexico, Ecuador, Peru, Brazil, Argentina, Saudi Arabia, Pakistan, Afghanistan, South Africa, United Kingdom, France, Spain, Switzerland, Australia and New Zealand.

Frozen: How the Revocation of the U.S. – Russia Tax Treaty Puts Global Trade on Thin Ice

Jack Brister

Founder, International Wealth Tax Advisors

Jack Brister, Founder of International Wealth Tax Advisors, is a noted international tax expert, with over 25 years of experience. Jack specializes in U.S. tax planning and compliance for non-U.S. families with international wealth and asset protection structures.

Jack is a frequent featured speaker at numerous international financial conferences and has been named a Citywealth Top 100 U.S. Wealth Advisor.

Contact IWTA

To schedule an introductory phone conference with IWTA founder Jack Brister simply clickhere. Email IWTA atbloginquiries@iwtas.com Or call the IWTA New York City office at 212-256-1142

Updated: May 18, 2022

We continue to monitor the U.S.-Russia tax treaty withdrawal along with economic and trade sanctions. It’s a constantly developing situation that profoundly affects global business and cross-border tax collection. Following is an update to IWTA founder Jack Brister’s article published in JD Supra on March 18, 2022.

New Developments

The Biden administration is poised to fully block Russia’s ability to pay U.S. bondholders. A temporary exemption deadline that gave Moscow leeway to pay coupons in dollars expires on May 25, 2022. The move could bring Moscow closer to the brink of default, Treasury sources told Bloomberg.

Tax Treaty Revocation in Action

The U.S. government had already been putting pressure on Russia. On April 5th the Treasury Department told multiple news outlets that it had suspended its tax information exchanges with Russia. That decision essentially blocks Russian authorities from obtaining tax information from the U.S. that would help their domestic collections, which could be a strong economic blow to the country.

Frozen: How the Revocation of the U.S. – Russia Tax Treaty Puts Global Trade on Thin Ice

Originally published on March 18, 2022 on JDSupra.

Permanent Normal Trade Relations (PNTR), commonly known as a nation’s most favored (MFN) status has been used in trade treaties for years. Using the MFN clause requires that a country that provides a trade concession to one trading partner must extend the same treatment to all of its partners. Used by the World Trade Organization the loss of this status can expose a country to discriminatory import tariffs.

Through the MFN status, the 164 members in the World Trade Organization treat each other equally, benefitting from highest import quotas, lowest tariffs and fewest trade barriers for goods and services. Members are allowed to impose whatever trade measures they wish on non- members, within reason. In addition, Biden announced that the G7 was seeking to ban Russia’s borrowing from the IMF and the World Bank. By revoking Russia’s MFN status, the United States and its allies send a strong signal that they no longer consider Russia an economic partner.

But the losses will go farther than Russia. The resulting tariffs will also raise costs for Americans and trading partners that may rely on affected Russian products. The United States is somewhat reliant on commodities exported from Russia, including fertilizers and base metals and the specific import restrictions will determine the impact of the sanctions.

What Are the Tax Implications of a Revoked U.S. – Russia Tax Treaty?

In tax treaties, the MFN clause promotes non-discrimination and parity for treaty partner countries. The main purpose of a tax treaty is to ensure proper tax treatment of monies earned by citizens, expats and residents of each other’s country. At present, the tax treaty between the United States and Russia is still in place, however, the US Senate Foreign Relations Committee has proposed a review of the US-Russia tax treaty.

Without the treaty, Russian investors with U.S.-sourced dividends would not only face a 30% withholding tax rate, they would also lose preferential treatment. The impact could be as great for American businesses in Russia as it is for Russian businesses. However, the ability to have offshore holdings in haven jurisdictions as well as the option of using cryptocurrencies for transactions, revocation of the tax treaty may not be as effective as it looks on paper..

Proposed tax changes aimed at penalizing the Russian government and Russians subject to sanctions who own U.S. assets is also in play. The plan, by Senate Finance Committee Chairman Ron Wyden (D., Ore.), would look to remove foreign-tax credits and certain deductions for U.S. companies earning income in Russia and Belarus.

We advise clients with business and investment ties to Russia to keep in touch as we continue to monitor the breaking developments in this unprecedented time of turmoil.

International Tax in 2022: The Year of Disclosure and Investment

Jack Brister

Founder, International Wealth Tax Advisors

Jack Brister, Founder of International Wealth Tax Advisors, is a noted international tax expert, with over 25 years of experience. Jack specializes in U.S. tax planning and compliance for non-U.S. families with international wealth and asset protection structures.

Jack is a frequent featured speaker at numerous international financial conferences and has been named a Citywealth Top 100 U.S. Wealth Advisor.

Contact IWTA

To schedule an introductory phone conference with IWTA founder Jack Brister simply clickhere. Email IWTA atbloginquiries@iwtas.com Or call the IWTA New York City office at 212-256-1142

International Tax in 2022:

The Year of Disclosure and Investment

For taxing authorities around the world, monitoring taxpayer disclosures and transparency will be a top line item in 2022, meaning taxpayers — especially high-net-worth individuals and corporate entities — should expect more scrutiny into their affairs. Governments are in a unique position as they navigate multiple demands and pressures. On one hand, the revenue demands of the COVID-19 economic recovery require creative strategizing, and lawmakers around the world are eyeing tax as a main driver. Increased public scrutiny on high-net-worth individuals due to data leaks like the Panama Papers and Pandora Papers is also placing more pressure on lawmakers to hold tax evaders to account. Throw in long simmering concerns about tax fraud, international money laundering and corruption, and it is apparent that taxing authorities will be focusing on how they can obtain more taxpayer information. At the same time, countries are also competing for foreign investment as part of their pandemic recovery strategy, and tax incentives for foreign investors will be a key area to watch in 2022.

New Rules: The U.S. Corporate Transparency Act

In the United States, Democratic and Republican lawmakers alike are concerned that the country’s millions of anonymous shell companies are enabling corruption, tax fraud, and money laundering. Those concerns drove Congress in January 2021 to enact a wide-sweeping beneficial ownership reporting law, the Corporate Transparency Act, which is one of the largest transparency-related laws in recent memory. The CTA was included in the National Defense Authorization Act for Fiscal Year 2021. In 2022, Treasury’s Financial Crimes Enforcement Network (FinCEN) will release three sets of implementing rules for the CTA that will impact millions of U.S. corporations, limited liability companies, and similar entities. Over the next few months, taxpayers will need to keep abreast of the rules as they are released by FinCEN and potentially participate in FinCEN’s regulatory notice and comment process as the office attempts to address several open issues within the law.

The CTA requires domestic and foreign “reporting companies” to send to FinCEN the names, addresses, dates of birth, and driver’s licenses or other identification numbers of their beneficial owners who have substantial control. But what is a reporting company? Or a beneficial owner? What does substantial control mean for purposes of the CTA? The first tranche of proposed FinCEN rules, which were published December 8, 2021, to provide some guidance.

The CTA applies to corporations, LLCs, and “other similar entities” and although the law doesn’t define “other similar entities” the December 8 proposed rules offer some insight.

A foreign reporting company is any entity formed under foreign law that is registered to do business within the United States. A domestic reporting company is any entity created by the filing of a document with a secretary of state or filed with a similar office within a U.S. jurisdiction, like a state.

In the proposed regulations, FinCEN wrote that the proposed definition of domestic reporting company “would likely include limited liability partnerships, limited liability companies, business trusts (aka statutory trusts or Massachusetts trusts) and most limited partnerships, in addition to corporations and limited liability companies,” because they typically are created by a filing with a secretary of state or similar office.

That definition will capture a lot of entities – there are about 30 million in the U.S. according to FinCEN’s estimation. Another 3 million are created annually. FinCEN said it does not plan to include any other legal forms other than corporations and LLCs within the definition, noting that U.S. state and tribal laws differ on whether other types of trusts and business forms like general partnerships are created by a filing.

There also are several exemptions, as the CTA exempts 23 different kinds of entities under 31 U.S.C. 5336(a)(11)(B)(i)-(xxiii). For example, FinCEN’s proposed regulations clarify that under the large company exemption, any domestic company or foreign entity that is registered to do business in the U.S. is exempt from the CTA’s reporting requirements if it meets the following hallmarks: (1) Over 20 full-time U.S.-based employees; (2) more than $5 million in gross receipts or sales from sources inside the U.S., as reflected on a U.S. federal income tax or information return; and (3) operates a physical office in the U.S.

The next question is, who is a beneficial owner with substantial control? The CTA defines a beneficial owner as “any individual who meets at least one of two criteria: (1) exercising substantial control over the reporting company; or (2) owning or controlling at least 25 percent of the ownership interest of the reporting company.” Under the CTA, substantial control is defined as: (1) service as a senior officer of a reporting company; (2) authority over the appointment or removal of any senior officer or dominant majority of the board of directors (or similar body) of a reporting company; and (3) direction, determination, or decision of, or substantial influence over, important matters of a reporting company.

Beyond that, the proposed regulations say that determining an ownership interest is a facts and circumstances inquiry that evaluates criteria such as: (1) equity in the reporting company and other types of interests, like capital or profit interests (including partnership interests), or convertible instruments; (2) warrants or rights; or (3) other options or privileges to acquire equity, capital, or other interests in a reporting company.

The stakes – and potential penalties – are high. Taxpayers that willfully fail to share beneficial ownership information with FinCEN face civil penalties of up to $500 per day. Criminal penalties can hit $10,000 per violation. Based on this, and the broad sweeping nature of the CTA, taxpayers who meet the criteria for domestic or foreign reporting companies or want to know if they are exempt, will want to explore their options with an experienced international tax professional.

High Net Worth Individuals: Wealth Tax VS Enforcement

Globally, wealth taxation has commanded quite a bit of attention as governments strategize ways to raise revenue in light of the COVID-19 pandemic. Some countries have been more active than others. For example, Singaporean lawmakers are considering a graduated net wealth tax between 0.5 and 2 percent imposed on individual net worth exceeding SGD 10 million (about $7.4 million). Norway’s Parliament at the end of 2021 passed a bill to increase the country’s wealth tax base rate from 0.85 percent to 0.95 percent. Taxpayers whose assets exceed NOK 20 million will be assessed at a 1.1 percent rate.

Meanwhile, in the U.S. and much of Europe, wealth taxes have failed to gain much traction. What has proven popular is an increased focus on tax enforcement. President Joe Biden placed tax enforcement as a cornerstone of his Build Back Better economic strategy, and he wants to increase the IRS’ funding by $80 billion. For over a decade significant budget cuts have eroded IRS enforcement capabilities and cost the government billions of dollars in uncollected taxes. The IRS funding plan, which is part of Biden’s now- stalled Build Back Better social spending bill, would give the IRS $80 billion over 10 years to ramp up its enforcement and investigative work, particularly on audits of corporations and wealthy taxpayers. See our recent article on Build Back Better.

In the United Kingdom, HM Revenue & Customs has increased its investigations into criminal and tax offenders, and that work has recovered over £1 billion over the past five years. HMRC plans to continue that work in 2022, and specifically plans to rely more heavily on its powers to freeze and recover unexplained assets. Judging by the department’s prior activity, that could be quite a bit of activity: between 2020 and 2021, HMRC issued 151 account freezing orders, covering over £26 million in assets.

In 2021, Spain decided to investigate high net worth individuals who move their tax domicile abroad to determine whether or not they are doing so fraudulently, and that activity will continue in 2022. The same is true in China. In late 2021, China’s State Tax Administration announced that it would launch investigations into high net worth individuals suspected of engaging in tax evasion. Developments like these suggest that high net worth individuals should prepare for increased scrutiny into their tax affairs and engage the help of a professional to prepare for potential inquiries.